The generative synthetic intelligence (AI) wave has boosted the prospects for numerous classes of corporations inside the tech sector, together with semiconductor makers, cloud computing suppliers, and cybersecurity gamers. Particularly, cloud computing corporations are witnessing stable demand for his or her companies which can be required to help enterprises and builders in constructing their generative AI fashions.

Bearing this favorable backdrop in thoughts, we used TipRanks’ Inventory Comparability Device to position Amazon (AMZN), Microsoft (MSFT), and Alphabet (GOOGL) towards one another to seek out the cloud computing firm that’s the greatest AI inventory and will provide the very best returns from the present degree, as per Wall Road analysts.

Microsoft (NASDAQ:MSFT)

Whereas Amazon Internet Companies (AWS) stays the market chief within the cloud infrastructure market, rival Microsoft Azure is catching up quickly. Within the March quarter (Q3 FY24 for MSFT), income from Azure and different cloud companies elevated 31% in comparison with AWS’ gross sales development of 17% within the comparable quarter.

Throughout the Q3 FY24 earnings name, Microsoft CEO Satya Nadella said that Azure is grabbing market share, with clients utilizing the corporate’s platforms to construct AI options. The CEO added that the corporate supplies a various choice of AI accelerators, together with the latest choices of Nvidia (NVDA), AMD (AMD), and MSFT’s personal AI chip.

Microsoft claims that over 65% of the Fortune 500 corporations are utilizing Azure OpenAI service, due to continued AI innovation that’s backed by the corporate’s strategic partnership with ChatGPT creator OpenAI. Total, Microsoft’s cloud enterprise is seen as certainly one of its key development drivers.

Is Microsoft a Purchase or Promote?

Microsoft is scheduled to announce its This fall FY24 outcomes on July 30. Analysts anticipate the corporate’s adjusted earnings per share (EPS) to rise 9% year-over-year to $2.93.

Forward of the outcomes, TD Cowen analyst Derrick Wooden reaffirmed a Purchase ranking on MSFT inventory and boosted the value goal to $495 from $470. The analyst expects the corporate to ship one other upbeat quarter of development and margins. He’s optimistic about Azure’s potential, with knowledge factors indicating continued development acceleration developments. Total, MSFT stays “best-positioned for AI monetization,” in response to Wooden.

With 34 Buys versus one Maintain advice, Microsoft inventory scores a Sturdy Purchase consensus ranking. The common MSFT inventory worth goal of $504.12 implies 15.3% upside potential from present ranges. Shares have superior greater than 16% to date this 12 months.

Amazon (NASDAQ:AMZN)

Regardless of rising competitors, Amazon’s AWS unit continues to keep up a dominant place within the cloud computing market. In keeping with Synergy Analysis Group, AWS commanded a 31% market share of the cloud infrastructure companies market in Q1 2024, whereas Microsoft Azure and Google Cloud had market shares of 25% and 11%, respectively.

Within the first quarter of 2024, AWS’ gross sales grew 17% year-over-year to $25 billion. This development charge marked an acceleration in comparison with the 13% improve skilled in This fall 2023. It’s price noting that AWS is a crucial development engine for Amazon and is very worthwhile. In Q1 2024, AWS accounted for 17.5% of the general gross sales however contributed greater than 61% of the corporate’s working earnings.

Amazon is optimistic concerning the sturdy potential of its AWS enterprise. CEO Andy Jassy said throughout the Q1 2024 earnings name that the corporate is seeing notable momentum on the AI entrance, which is accumulating a “multibillion-dollar income run charge already.”

What’s the Goal Worth for Amazon Inventory?

Forward of Amazon’s Q2 outcomes scheduled to be introduced on August 1, analysts at Morgan Stanley reaffirmed a Purchase ranking on the inventory, with a constructive near-term outlook. Morgan Stanley expects AMZN to report a notable EBIT (earnings earlier than curiosity and taxes) beat within the second quarter and challenge favorable steerage for the third quarter.

Particularly, Morgan Stanley’s EBIT estimate is 17% larger than the Road’s consensus for Q2 and 10% greater than the Q3 forecast. The optimistic outlook is predicated on AMZN’s North America Retail profitability and accelerating AWS development. In the meantime, Wall Road expects Amazon’s EPS to extend to $1.02 from $0.65 within the prior-year quarter.

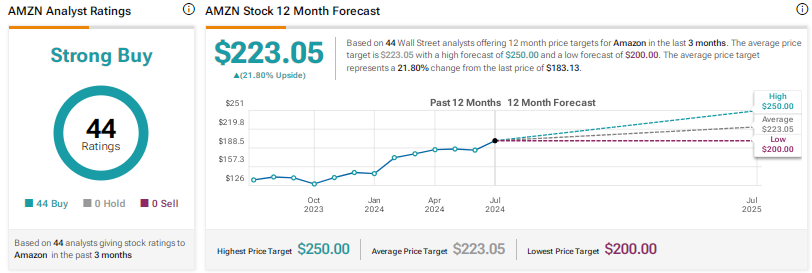

Amazon inventory earns a Sturdy Purchase consensus ranking primarily based on 44 unanimous Buys. At $223.05, the typical AZMN inventory worth goal implies about 22% upside potential. Shares have risen 21% year-to-date.

Alphabet (NASDAQ:GOOGL)

Tech large Alphabet is well-known for its Google search engine. That stated, the corporate’s Google Cloud enterprise is grabbing Wall Road’s consideration with its fast development. Alphabet impressed traders with its stable first-quarter outcomes, which have been pushed by a serious bounce in Google Cloud’s profitability.

In Q1 2024, Google Cloud’s income elevated 28.4% year-over-year to $9.57 billion, whereas its working earnings surged to $900 million from $191 million within the prior-year quarter. The outcomes mirrored Alphabet’s elevated investments within the Cloud enterprise. Curiously, throughout the Q1 2024 earnings name, administration highlighted that the corporate launched over 1,000 new merchandise and options in its Cloud enterprise over the previous eight months.

The corporate believes that one of many elements that differentiates its Cloud enterprise from rivals is its AI Hypercomputer, which gives cost-effective and environment friendly infrastructure to coach and help AI fashions.

Is it a Good Time to Purchase GOOGL?

On July 18, analysts at Jefferies reaffirmed a Purchase ranking on GOOGL inventory with a worth goal of $220. They anticipate Alphabet to report sturdy Q2 outcomes, supported by resilient buyer spending and constant Cloud enterprise. Nonetheless, Jefferies cautioned traders about barely harder comparisons in Q2, primarily within the advert enterprise.

After a stable year-to-date rally in GOOGL inventory (up 27.2%), Jefferies expects continued rise however at a gradual tempo because of excessive expectations following sturdy Q1 efficiency and above historic common valuation ranges.

Alphabet will announce its Q2 2024 outcomes on July 23. Wall Road expects Alphabet’s Q2 EPS to rise 27% to $1.83.

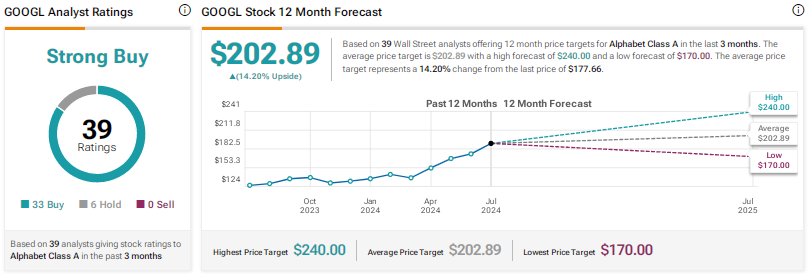

Wall Road has a Sturdy Purchase consensus ranking on GOOGL inventory primarily based on 33 Buys and 6 Holds. The common GOOGL inventory worth goal of $202.89 signifies 14.2% upside potential from present ranges.

Conclusion

Wall Road is bullish on the long-term development potential of the highest three cloud computing gamers, pushed by the continued transition of enterprises to the cloud and AI-related tailwinds. At the moment, they see barely larger upside potential in Amazon inventory than in Microsoft and Alphabet shares. Except for the enticing development potential of the AWS enterprise, analysts’ optimism about Amazon can be backed by the corporate’s management in e-commerce and its rising promoting enterprise.

RelatedPosts

")

{kind=link}