IONOS Group SE (ETR:IOS) got here out with its first-quarter outcomes final week, and we needed to see how the enterprise is performing and what trade forecasters consider the corporate following this report. Revenues got here in 3.1% beneath expectations, at €373m. Statutory earnings per share have been comparatively higher off, with a per-share revenue of €1.23 being roughly in step with analyst estimates. Following the outcome, the analysts have up to date their earnings mannequin, and it could be good to know whether or not they assume there’s been a robust change within the firm’s prospects, or if it is enterprise as normal. With this in thoughts, we have gathered the newest statutory forecasts to see what the analysts predict for subsequent 12 months.

See our newest evaluation for IONOS Group

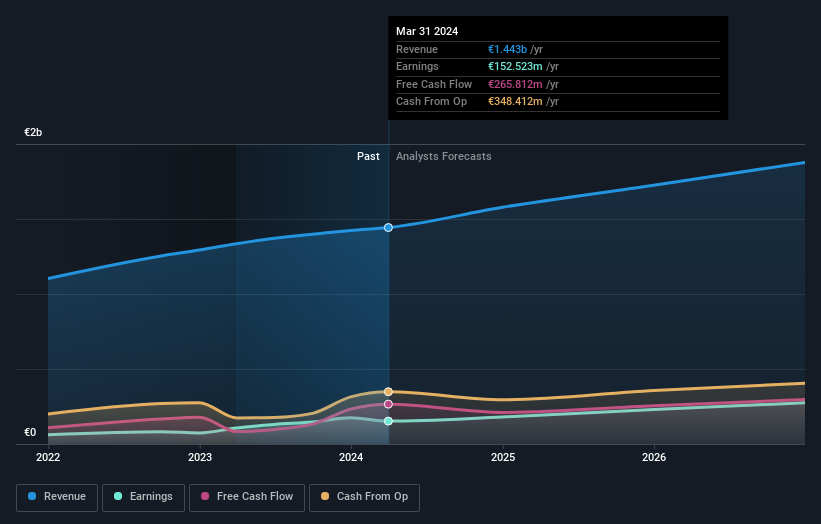

Following the newest outcomes, IONOS Group’s 9 analysts are actually forecasting revenues of €1.58b in 2024. This may be a significant 9.4% enchancment in income in comparison with the final 12 months. Statutory earnings per share are predicted to ascend 18% to €1.29. But previous to the newest earnings, the analysts had been anticipated revenues of €1.58b and earnings per share (EPS) of €1.29 in 2024. The consensus analysts do not appear to have seen something in these outcomes that might have modified their view on the enterprise, given there’s been no main change to their estimates.

The analysts reconfirmed their value goal of €26.27, exhibiting that the enterprise is executing nicely and in step with expectations. The consensus value goal is simply a mean of particular person analyst targets, so – it may very well be helpful to see how vast the vary of underlying estimates is. Presently, probably the most bullish analyst values IONOS Group at €28.00 per share, whereas probably the most bearish costs it at €23.20. The slender unfold of estimates may recommend that the enterprise’ future is comparatively simple to worth, or thatthe analysts have a robust view on its prospects.

Wanting on the larger image now, one of many methods we are able to make sense of those forecasts is to see how they measure up towards each previous efficiency and trade progress estimates. The analysts are undoubtedly anticipating IONOS Group’s progress to speed up, with the forecast 13% annualised progress to the top of 2024 rating favourably alongside historic progress of 8.1% each year over the previous 12 months. Examine this with different firms in the identical trade, that are forecast to develop their income 9.0% yearly. It appears apparent that, whereas the expansion outlook is brighter than the current previous, the analysts additionally anticipate IONOS Group to develop sooner than the broader trade.

The Backside Line

Crucial factor to remove is that there is been no main change in sentiment, with the analysts reconfirming that the enterprise is performing in step with their earlier earnings per share estimates. Fortuitously, additionally they reconfirmed their income numbers, suggesting that it is monitoring in step with expectations. Moreover, our knowledge means that income is anticipated to develop sooner than the broader trade. There was no actual change to the consensus value goal, suggesting that the intrinsic worth of the enterprise has not undergone any main adjustments with the newest estimates.

With that mentioned, the long-term trajectory of the corporate’s earnings is much more vital than subsequent 12 months. We have now forecasts for IONOS Group going out to 2026, and you’ll see them free on our platform right here.

Even so, bear in mind that IONOS Group is exhibiting 1 warning register our funding evaluation , it’s best to learn about…

Have suggestions on this text? Involved concerning the content material? Get in contact with us immediately. Alternatively, electronic mail editorial-team (at) simplywallst.com.

This text by Merely Wall St is normal in nature. We offer commentary primarily based on historic knowledge and analyst forecasts solely utilizing an unbiased methodology and our articles should not supposed to be monetary recommendation. It doesn’t represent a suggestion to purchase or promote any inventory, and doesn’t take account of your targets, or your monetary scenario. We purpose to carry you long-term targeted evaluation pushed by elementary knowledge. Notice that our evaluation might not issue within the newest price-sensitive firm bulletins or qualitative materials. Merely Wall St has no place in any shares talked about.